Algo Trading: When Code Replaces the Trader

In modern finance, most of the action isn't happening on a trading floor, it's happening in computer servers. Algorithmic Trading (Algo Trading) is the execution of trade orders automatically based on pre-programmed instructions that factor in price, volume, and time. This field, where Computer Science directly controls billions, is the pinnacle of FinTech.

Algo trading isn't just for Wall Street firms anymore. The goal is simple: eliminate human emotion and execute trades faster and more precisely than any person ever could.

Backtesting, ML, and the Race for Low Latency

Algorithmic trading relies on two critical engineering disciplines:

1. Data Science & Backtesting: Algorithms are worthless without proof. Backtesting involves running a strategy against vast amounts of historical market data to measure its performance before risking real money. Today, many strategies use Machine Learning models (e.g., RNNs, LSTMs) to predict price movements based on complex, non-linear relationships in the data.

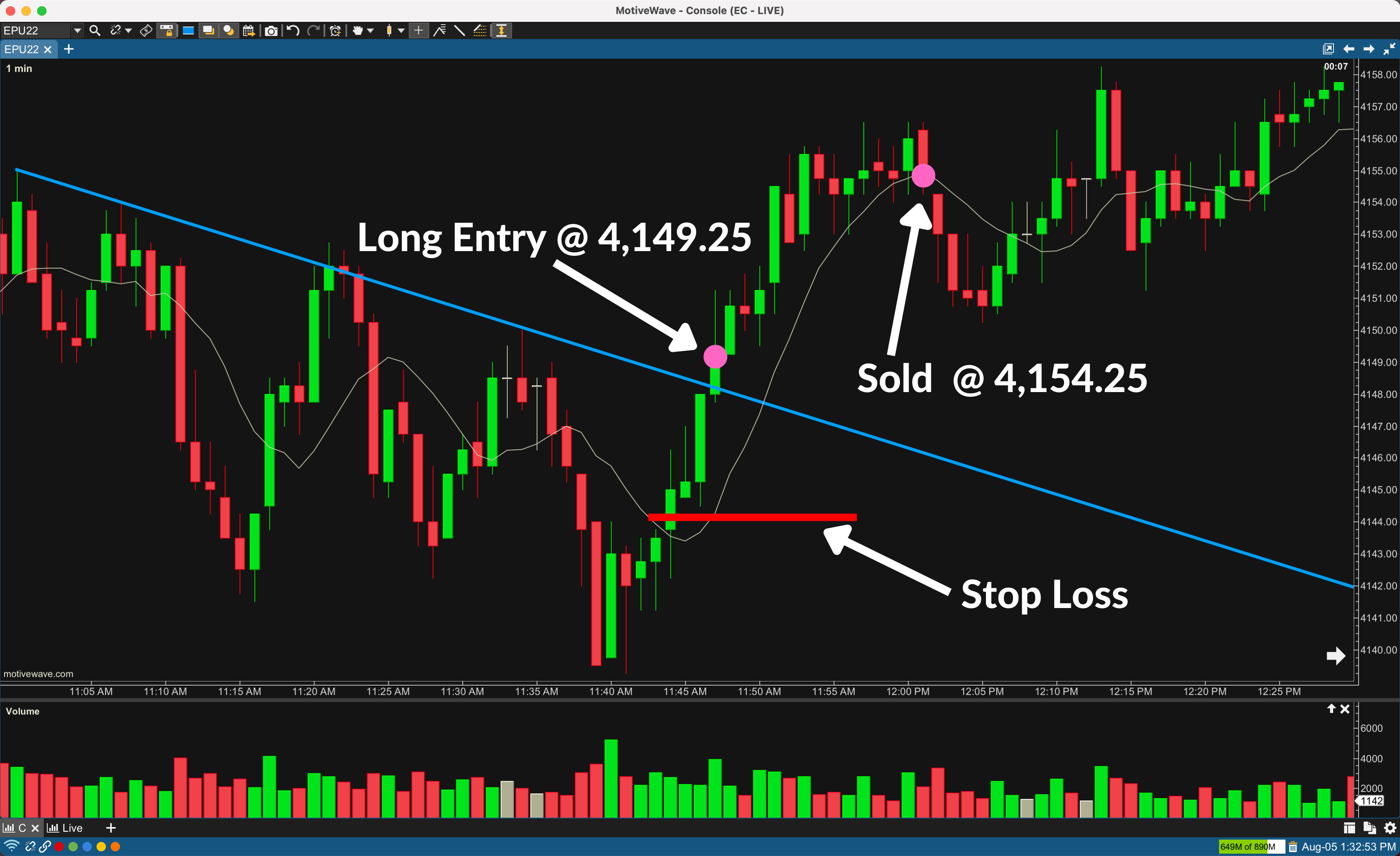

The Microsecond Race: Low Latency and HFT

For strategies that execute thousands of trades per second, known as High-Frequency Trading (HFT), microseconds matter. This is pure performance engineering. Algo developers build ultra-optimized systems using specialized hardware, optimized network routing, and high-performance languages like C++ and Rust to ensure the trade order reaches the exchange faster than the competition.

In HFT, being just a fraction of a second slower than a competitor means guaranteed loss. This is the ultimate challenge in distributed and systems programming.

The Critical Guardrail: Risk and Strategy Types

No strategy works without Risk Management. Engineers must code rules to protect capital. Key risks include Slippage (the difference between the expected and actual execution price) and Drawdown (the maximum loss from a peak in capital). Algo strategies generally fall into a few buckets:

Arbitrage: Exploiting tiny price differences between different exchanges.

Conclusion: Building Your First Bot and Key Skills

The intersection of Computer Engineering and Finance offers the ultimate high-stakes challenge. Your best starting point is the classic Moving Average Crossover strategy, which you can easily code using Python (Pandas for data, backtesting libraries like Zipline).

Key Skills to Master for an Algo Career:

1. Python (for research and backtesting)

2. C++ / Rust (for low-latency execution)

3. Probability, Statistics, and Time-Series Analysis.

If you want your code to directly move markets, start mastering the math and the systems today.

Tanvi Patange